Overview

Understanding mortgage rates is crucial for home buyers as these rates directly impact the overall cost of your home loan. Whether you’re looking at current mortgage rates or exploring options like a 30-year mortgage rate or a 20-year fixed rate mortgage, being informed about how these rates are determined and what factors influence them can help you make better financial decisions.

Tools like a mortgage recast calculator or a recast mortgage payment calculator can assist in planning your payments effectively, potentially saving you money over the life of your loan.

In today’s market, knowing the mortgage rates today and understanding the interest rates today can give you a clear picture of the financial landscape. By using a mortgage recast calculator, you can explore how adjusting your loan payments might impact your long-term costs. Whether you’re a first-time homebuyer or looking to refinance, keeping an eye on the current mortgage rates and using tools like the recast mortgage payment calculator can help you navigate the complexities of home financing.

What is a Mortgage Rate?

A mortgage rate is the interest rate charged by a lender for borrowing money to purchase a home. It determines how much you will pay in interest over the life of the loan. Mortgage rates can be fixed or adjustable and significantly impact your monthly payments and the total cost of the loan.

A mortgage rate is the interest rate charged by a lender on a mortgage loan. This rate determines the cost of borrowing money to purchase or refinance a home and is expressed as a percentage.

Mortgage Rate Definition: A mortgage rate is essentially the cost of borrowing money expressed as a percentage of the loan amount. It affects your monthly mortgage payments and the overall amount paid in interest over the term of the loan.

In other words, a mortgage rate is the cost of borrowing money to buy a home, expressed as a percentage of the loan amount. It determines how much you’ll pay in interest over the life of the loan and can be fixed or adjustable based on market conditions and the terms of your loan agreement.

Read Also: Home Buying Guide: Essential Tips for Your First Perfect Purchase

How Mortgage Interest is Calculated

a. Monthly Calculation

Mortgage interest is generally calculated on a monthly basis. The interest for each month is determined by multiplying the remaining principal balance by the monthly interest rate. You can check online calculator for more insight

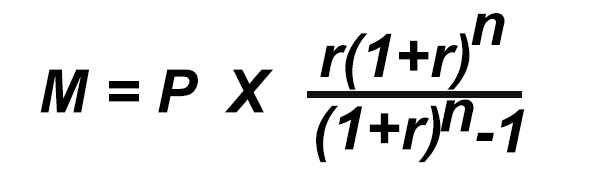

How is Mortgage Interest Calculated Per Month?

To calculate your monthly mortgage payment, you use the formula:

Where:

- MMM = Monthly payment

- PPP = Principal loan amount

- rrr = Monthly interest rate (annual rate divided by 12)

- nnn = Total number of payments (loan term in years multiplied by 12)

Mortgage Interest Example: For a $300,000 mortgage at a 4% annual interest rate over 30 years, the monthly payment would be approximately $1,432.25.

Read Also: Tenant Screening: 15 Essential Tips for Effective Screening

b. Daily vs. Monthly Compounding

Most mortgages use monthly compounding. This means that interest is calculated and added to the principal balance once a month.

Is Mortgage Interest Calculated Daily or Monthly?

Standard mortgages typically use monthly compounding. However, some lenders may offer daily compounding, where interest is calculated on a daily basis and added to the principal.

How Mortgage Interest Works

Mortgage interest is applied to the remaining principal balance of the loan. Initially, a larger portion of your monthly payment goes toward interest, and as you pay down the principal, a larger portion goes toward the principal.

How Does Mortgage Interest Work Example?

For a $250,000 mortgage at a 5% interest rate, your early payments will primarily cover interest. As you reduce the principal over time, the interest portion of your payments decreases.

Evaluating Mortgage Rates

1. Fixed vs. Adjustable Rates

Is a 3.75% Mortgage Rate Good?

A 3.75% rate is generally considered favorable, especially if market rates are higher. Compare it with current rates and consider your financial situation to determine if it’s good for you.

What Does a 6.5% Mortgage Rate Mean?

A 6.5% mortgage rate indicates a higher cost of borrowing compared to lower rates. This means higher monthly payments and more total interest paid over the life of the loan.

Is 6% a Bad Mortgage Rate?

A 6% rate is on the higher end compared to historical averages. It may not be ideal, especially if lower rates are available.

How Much of a Difference is 1% on a Mortgage?

A 1% difference in the interest rate can significantly affect your monthly payment and total interest paid. For example, on a $300,000 loan, a 1% increase can raise your monthly payment by about $180.

What is a Decent Mortgage Rate?

A decent mortgage rate depends on the current market conditions. Rates below 5% are generally considered good, but always compare offers from multiple lenders.

What is a Good Mortgage Rate for a 30-Year Fixed?

As of now, a good rate for a 30-year fixed mortgage might range between 5% and 6%. Always check current rates and market trends.

Read Also: 20 Essential Tips for Successful Landlords and Property Management in 2025

2. Understanding Mortgage Costs

How Much Will I Pay in Interest on My Mortgage Over 30 Years?

For a $300,000 mortgage at a 4% interest rate over 30 years, you’ll pay approximately $215,000 in interest. This varies based on the interest rate and loan amount.

What is the Average Mortgage on a $300,000 House?

The average mortgage payment for a $300,000 house will depend on the interest rate, loan term, and down payment. Using a 4% rate, the payment might be around $1,432.25 per month for a 30-year loan.

How Much Income Do I Need for a $200K Mortgage?

A general rule is that your mortgage payment should not exceed 28% of your gross monthly income. For a $200,000 mortgage, you might need an income of around $8,000 per month, depending on other debts and expenses.

Read Also: Real Estate Investment: Top 10 Affordable Neighborhoods to Invest

Mortgage Rate Trends and Predictions

Will Mortgage Rates Drop in 2024?

Predicting future rates is challenging. Economic forecasts, Federal Reserve policies, and market conditions will influence mortgage rates. Staying informed through reliable sources is essential.

What Will the Mortgage Rate Be in 2025?

Forecasting rates for 2025 involves speculation based on current trends and economic indicators. Market conditions and Federal Reserve actions will play a significant role.

Will Mortgage Rates Go Down to 3% Again?

It’s uncertain if rates will return to 3%. While rates may fluctuate, they depend on broader economic factors and monetary policies.

Refinancing and Rate Locking

What is the Average Cost to Refinance a Mortgage?

Refinancing typically costs between 2% and 5% of the loan amount. This includes fees such as application, appraisal, and closing costs.

Should I Lock My Mortgage Rate Today?

If you find a favorable rate, locking it in can protect you from potential rate increases. Consider the terms of the lock and your home-buying timeline.

Read Also: The Pros and Cons of Short-Term vs. Long-Term Rentals

Mortgage Rate Optimization

What Type of Mortgage Loan Has the Lowest Interest Rate?

Adjustable-rate mortgages (ARMs)

Adjustable-rate mortgages (ARMs) often offer lower initial rates compared to fixed-rate mortgages. However, the best option depends on your financial situation and tolerance for rate fluctuations.

Adjustable-rate mortgages (ARMs) are home loans with interest rates that can change periodically based on market conditions. Unlike fixed-rate mortgages, where the interest rate remains constant throughout the loan term, ARMs have rates that can fluctuate, impacting your monthly payments.

Key Features of ARMs:

- Initial Rate: ARMs typically start with a lower interest rate compared to fixed-rate mortgages, known as the initial or introductory rate. This rate is fixed for a specific period, such as 1, 3, 5, or 7 years.

- Adjustment Periods: After the initial rate period ends, the interest rate adjusts at regular intervals, which can be annually, semi-annually, or according to another schedule. The new rate is based on a benchmark index plus a margin set by the lender.

- Index and Margin: The rate adjustments are tied to a specific financial index, like the LIBOR (London Interbank Offered Rate) or the Treasury Index. The lender adds a margin to this index to determine the new rate. For example, if the index is 2% and the margin is 2%, the new rate would be 4%.

- Caps and Floors: ARMs often have caps that limit how much the interest rate can increase or decrease at each adjustment period and over the life of the loan. Floors are the minimum rate the mortgage can reach.

- Payment Changes: As the interest rate changes, your monthly payments can vary, which can affect your budget and financial planning.

ARMs can be beneficial if you plan to move or refinance before the rate adjusts, as they often offer lower initial rates. However, they carry the risk of higher payments if interest rates rise.

What is the Math for Mortgage Rates?

The APR calculation includes the loan amount, interest rate, and fees, providing a clearer picture of the total borrowing cost. Online calculators can help with precise calculations.

What is the Golden Rule of Mortgage?

The golden rule is to ensure that your monthly mortgage payments are manageable within your budget and that you maintain a healthy debt-to-income ratio.

What is a Good Credit Score for a Mortgage?

A credit score of 700 or higher is generally considered good for obtaining favorable mortgage rates. Higher scores can help you secure the best rates available.

Conclusion

Understanding mortgage rates is essential for making informed home-buying decisions. By knowing how rates are calculated, the types of rates available, and how to secure the best rate, you can better manage your home financing. Stay updated on current rates, improve your credit score, and consider your long-term financial goals to ensure a successful home purchase.

Ready to find the best mortgage rate for your new home? Start by comparing rates from multiple lenders and consult with a mortgage advisor to make an informed choice. If you found this guide helpful, share it with friends and family who might be in the market for a new home. For more expert advice and tips on real estate, subscribe to our newsletter or explore our other resources on foreclosures. Your dream home is just a smart mortgage away!